Top 12 White-Label Solutions for Neobanks in 2026

The banking sector has evolved considerably over the past decade, with the gradual adoption of innovative digital technologies being the main driver of digitalization. Thus, around 40% of top banks across the globe are launching the BaaS service in an effort to retain the tech-savvy customer base and diversify their revenue streams in the coming years. The pressure to go digital is even more significant amid the talks that 85% of traditional banking services will disappear over the next decade because of obsolescence.

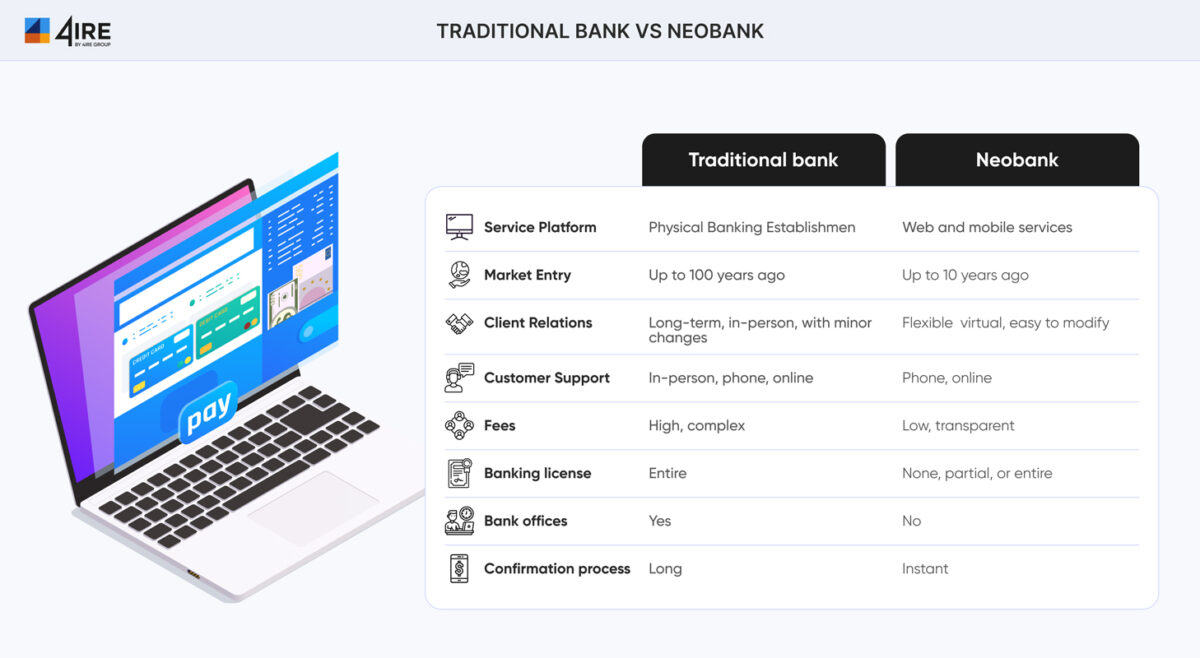

The new banking model that gains momentum amid these changes is Neobank – an innovative, online-only banking entity providing a top-quality digital user experience across the entire spectrum of financial operations. Neobanks are mobile-first apps handling payments, money transactions, loans, and many other services with unrivaled speed and affordability.

According to Statista’s 2025 report, neobank transactions reached $7.8 trillion, up 21% from 2024, with a forecast to grow to $12 trillion by 2029 (CAGR 23%). Besides, the number of active Neobank clients is expected to reach 386 million users, giving the Neobank model over 4.82% of user penetration. The recent Neobank startups have been highly successful, such as the UK-based Zopa bank, raising over $95 million in funding, the Brazilian Nubank, Chime, Current, and Aspiration, among others.

As you can see, the banking landscape is ripe for change, further accelerated by 5G and massive smartphone access among users globally. Thus, building a Neobank today is an idea with immense market potential and a healthy ROI for years to come.

What Is a Neobank?

A neobank is a digital financial company that provides banking services exclusively through online and mobile platforms, without any physical branches. By eliminating the costs of traditional banking, neobanks can offer more cost-effective financial solutions to their customers. How to launch a neobank? Starting a neobank is relatively simple, with its main feature being the provision of financial services through P2P payment applications, typically optimized for use on mobile devices.

While it might sound so, neobanks do not replace the usual banking services; they rather enhance the existing offer in the market by heavily integrating modern technological advancements. Besides differing from the traditional and union banks, the neobanks are also unlike online banks. The latter, while not having a physical representation, still remain a part of a country’s financial system and abide by the laws of their country of origin. Neobanks, in their turn, have the following features:

- Lack of connection to any state or federal bank regulations

- Provision of mainly mobile services

- Close cooperation with traditional banks

- Lack of extended credit

How Neobanks Work?

A neobank can be regarded as an app on a mobile device that helps to manage a user’s finances. It has the traditional approach of an app – a user needs to register to begin using the app. Such applications frequently offer financial educational services, like budget planners. However, if a customer wants to manage their bank account and pay through the neobank with the money stored in a traditional bank, the provision of additional personal data (connection of the bank account) will be essential.

From a technological perspective, it is an application that offers financial services: from small loans to savings accounts. Some providers would have signed cooperation agreements with traditional banks in order to gain access to users’ financial data and have a wider spectrum of services, such as payment and money transferring.

To lower their risks and also keep the operational costs to a minimum, neobanks tend not to offer any loans; yet, some exceptions can be found in the market, mostly in Australia, where most neobanks offer even home loans.

The Pros and Cons of Neobanks

While many people use internet-based tech perks every day, there are still skeptics of the apps in general; these customers frequently do not believe in the internet and do not trust technology when it comes to their finances. This lack of trust in neobanks is completely ungrounded. Even though these are not official banks under federal or state regulations for traditional banking services, there are still regulatory bodies in every country that control and monitor the operations of such entities. For example, in the US, the FDIC would need to certify the service, while in Australia, a neobank needs to have an ADI license issued by APRA. So the advantage number one – neobanks are secure, and frequently even more than traditional banking offers. All you need to do is ensure that the selected neobank is licensed or certified by the respective body in your country.

Besides that, here is a list of advantages a neobank can offer:

- Low costs: most products and services in neobanks have no monthly maintenance fee and generally cost less than in traditional institutions.

- Convenience: for the tech-smart people, neobanks offer all banking services within a single app + the ability to manage the finances at any time of day and night, provided that the user has a smartphone with an internet connection.

- Fast processing time: there is no need to wait for the card to arrive in a week via post; neobank allows you to set up an account in a few minutes and to begin using the service (loan, payment, advice) right away.

- AI-Driven Personalization: Neobanks can engage users and contribute to their financial literacy with the help of smart AI tools, including budgeting and personalized financial analysis.

Of course, any service existing today has its downside; for neobanks, it is:

- Tech component: to use a neobank, a customer needs to have a phone, an internet connection, and generally feel comfortable with technology.

- Fewer regulations: this leads to greater risks when it comes to disputes. If the selected neobank is not trustworthy and there is a problem, there is less governmental support in a dispute with this provider compared to traditional banks.

- No physical representation: yes, neobanks allow completing all financial operations online. However, if a customer prefers having an eye-to-eye conversation with a representative in a branch, this might be a downside of neobanks, even though the customer service of these applications is robust. Still, 24/7 availability of customer support via multiple convenient channels is meant to overcome this downside.

- Cybersecurity risks: Neobanks are more susceptible to cyber threats because of their digital architecture. One notorious example is the 2024 Revolut data breach, which fueled further discussions of the need to implement biometric access and move banking operations to blockchain. These advanced security technologies hold a promise for effective prevention of security incidents.

Neobanking Trends

Though Neobanks are a relatively innovative banking technology, they also can’t escape the fast pace of digital innovation and change. Here is a glimpse of the dominant neobanking trends that will shape the market in the coming years:

- AI-powered personalization. Neobanks are actively integrating AI tools to personalize their services and automate credit scoring for lending applications. Some successful examples of such innovations include Chime’s AI tool for real-time transaction analysis, which helps develop optimal savings plans for individual users, and the AI-powered predictive financial advice offered to Monzo users.

- Embedded finance. This concept stands for the integration of financial services into non-financial resources, including e-commerce or gaming platforms. Embedded solutions are meant to improve user experience and provide instant, omnichannel access to banking services. Some examples include the Cash App’s partnership with Sutton Bank and Marqeta for the provision of debit cards and embedded payment solutions, as well as the AI-driven Botim Ultra app by Quantix that automates credit scoring for a variety of businesses.

- Sustainability/ESG. More and more Neobanks integrate environmental, social, and governance (ESG) principles by providing green finance products and sustainable investment instruments. For example, the German Tomorrow Bank allows automated climate project funding from the app, and Revolut offers ESG-compliant investment options to users.

- Crypto and blockchain. Neobanks are the first in the banking sector to open access to crypto purchases and trading to their users. Some examples include Revolut and Zumo, both of which allow operations with crypto and support crypto investments.

- Emerging markets. Many developing regions, such as Africa or Latin America, have fragmented or flawed traditional banking infrastructures and high portions of mobile-friendly populations. Therefore, Neobanks spread rapidly in emerging markets due to their mobile-first interfaces and greater agility and accessibility of financial services compared to traditional banks. An illustrative example is Nubank – a Neobank that serves 46% of the adult population in Brazil.

- Open banking. Neobanks expand their service coverage and establish strategic partnerships using open banking APIs. Thus, financial ecosystems grow to offer investment, insurance, and analytics services alongside classical financial coverage. Some examples of such ecosystems include the American SoFi platform and the European Treezor BaaS service.

These and other trends are changing the present-day banking landscape and improving business performance along with customer experience across multiple dimensions. They reflect Neobanks’ continuous effort to meet the evolving consumer needs and disrupt traditional banking models.

What Is White-Label Banking?

To define what white-label banking is, it is essential to introduce a couple more definitions.

- Open banking is a practice that allows third parties to access the financial data of a bank. The main goal of open banking is to break the vicious circle of almost unlimited control of traditional banks over their customers. Open banking allows customers to select their financial services providers, hence taking greater supervision of their own finances.

- Bank as a service (BaaS) – the system in which traditional banks open their APIs to third parties and allow the use of this data to create new financial solutions to give customers a more convenient way to manage their resources.

Now that the founding concepts are clear, let’s review what white-label banking is. This new idea is clearer in the graph below.

The diagram above demonstrates that white-labeling solutions take the BaaS concept to the next level, where banking service is offered by a third-party company whose technology is based on someone else’s solution. The trick here is that the end-customer would generally not be aware that the app or software they are using is based on some other technology that exists in the market, since it would normally be rebranded to fit the marketing strategy and the end company.

Who Uses White–Label Financial Solutions?

Most frequently, the white-label software is used by traditional banks that do not want to (or maybe cannot) develop a decent software solution for their services. They then need to use some other company’s technology under their branding name to keep their existing clients and seem modern and up-to-date.

However, since neobanks are solely focused on providing financial services online, and mostly on mobile devices, they are also common users of the white-label financial products. Smaller challenger banks also purchase such solutions from fintech startups, rebrand them, and introduce them into their offer.

By default, a white-label solution developer provides full support for its software and, in rarer cases, might even run their software for a third party. And since white-label banking solutions are designed to facilitate the management of finances for the end-users, it means that legally, these are not banking services, hence they can be used by non-banks as well.

Benefits of White-Label Banking

Customers go for white-label solutions for three reasons:

- Flexibility: Fixed and uncomfortable rules already exist with traditional banking, so when it comes to the know-how options, they must be better! Flexibility in this respect applies both to the services offered to the end-customers – users of the software or app – as well as companies who will be implementing the white-label solution under their brand.

- One-size-fits-all service: A white-label solution provider is offering a SaaS, not a fixed product that must only fit the frame of the brand in its existing shape. A white-label solution is an idea of a service that is heavily customizable for the client; this is why the service itself basically can fit any need of a bank, neobank, challenger, or financial solution. The service here includes:

- Service rebranding.

- Qualitative onboarding.

- Help materials with clearly defined user journeys.

- Professional tech support.

- Continuing maintenance and updates whenever needed.

- Customer experience: Yes, a white-label solution exists for the sole purpose of providing a better experience than the existing market offers. So, a customer-centric approach with the VOC technologies is what takes such services one step ahead of the traditional financial system.

- App/software must be available for all OSs and browsers (for web solutions).

- No bugs and glitches. It must be perfect.

- Seamless integration with other services (banks, supporting systems).

Top White-Label Banking Services

The top services white-label baking solutions provide include:

- Accounts management

- Balance tracking

- Savings and checking accounts

- Deposits and withdrawals

- Virtual card issuance

- Simplified bill payments

- Insurance quotes

- Mortgages and personal loans

- Online payments and transfers

The List of 12 Best White-Label Solutions for Neobanks

The number of FinTech companies globally has grown from 12,000 in 2019 to 29,955 in 2024, and this growth continues into 2026 thanks to innovations in digital banking. Considering that EMEA takes a great percentage of all FinTech, our main selection of the white-label solutions for neobanks is focused on Europe’s offer and the Nordics in particular. However, at 4IRE, we appreciate the great solutions, so here is the list of the best products for neobanks globally:

1. NeobankX

NeobankX is a state-of-the-art modular solution that allows quick Neobank deployment. It’s a white-label, cloud-based FinTech platform suitable for businesses wishing to work with both fiat and crypto assets. The software scales seamlessly to cater to up to 10 million users per project and is compliant across jurisdictions. The main features for businesses include quick, frictionless integration of 30+ payment gateway options, automated KYC/AML procedures, multi-currency account setup, and real-time financial analytics.

Businesses using the NeobankX system can reap the following benefits:

- Scalable and reliable architecture developed by the industry’s top architects.

- A modular system with unlimited customization options and module addition on demand.

- A Neobank can be launched either as a crypto and fiat project or as a fiat-only digital bank with an opportunity to add cryptocurrency support later.

- On-premises deployment with ownership rights and digital architecture possession.

Due to its modular design, NeobankX reduces the project’s time to market to under 2-3 months. It’s not currently available as a SaaS solution, but its development is in the works. Therefore, it is an optimal solution for Neobanks that target a quick market entry and strategize for global reach.

2. CryptoBank

The CryptoBank white-label software is the proprietary product of the 4IRE team, specializing in crypto banking solutions. The solution is a blockchain-centric platform that allows Neobanks to expand their service coverage to digital assets and offer secure, efficient digital services. The product condenses the expertise and talent of 4IRE’s 250+ developer family and embodies the company’s firm grasp of FinTech analytics, development, and market research.

Appealing features of 4IRE’s CryptoBank solution include:

- Support for crypto trading and transactions with crypto.

- Provision of virtual IBANs to users.

- Branded card issuance.

- Time to market takes only 3-4 months.

- Support for 20+ blockchain and transaction cost reduction by 40%.

This product joins 4IRE’s extensive software product line that currently includes customizable mobile wallet solutions, user-friendly back-office tools, and personalized consulting services. The customizable back-end core of the CryptoBank makes software development smooth and flexible to your specific business needs, and broad support of integrations lets you create a fully unique and branded product. The white-label solution combines customization with a wide range of pre-configured, functional modules, thus enabling a quick startup for your banking project.

3. White-Label Digital Wallet Solution by RNDpoint

Another customizable white-label platform for Neobanks on our list is the product by RNDpoint. The solution is built using the low-code ProcessMIX platform, which allows quick and flexible back-end customization with minimal tech expertise. The product comes with a modular back-end, which speeds up the interface design without functionality limitations and guarantees rapid deployment in the fast-paced, competitive market.

RNDpoint’s solution comes with the following advantages:

- The project’s time to market is 3-4 months.

- The digital wallet supports multiple currencies and enables a multi-currency account setup.

- Clients can issue cards to their users.

- AI-powered algorithms take care of GDPR compliance and meet PCI DSS standards in real time.

- The White-label, modular design of the solution cuts down the development costs.

- The mobile user interface can be fully customized to your feature set and branding.

- A wide range of integrations is supported, with full back-end core customization.

- Cross-jurisdictional compliance is guaranteed by automated KYC/AML protocols.

The white-label digital wallet isn’t available as a SaaS solution.

4. ABLE Platform

The ABLE Platform is an all-in-one lending automation solution designed to help neobanks optimize their lending operations. It provides end-to-end automation, managing the entire loan lifecycle from origination to repayment. Neobanks can deploy the platform in just 1-2 months, significantly reducing time to market for new products. With its low-code architecture, ABLE allows full customization of workflows, dashboards, and interfaces to suit specific business needs.

The platform helps cut operational costs by up to 70%, offering a more efficient and scalable approach to lending. Its AI-powered credit scoring system ensures faster and more accurate risk assessments, improving decision-making. Built-in compliance features make it easier to meet regulatory requirements in different markets. The platform also supports seamless integration with third-party services for a unified user experience. Neobanks can expand their offerings with diverse loan products, including BNPL, personal loans, and microlending.

- Loan Origination Software

- Debt Collection Software

- BNPL Software

- Loan Management Software

- Credit Scoring Software

5. HES FinTech

HES FinTech offers an all-in-one lending automation platform for alternative lenders, fintech companies, and neobanks. It streamlines the entire loan lifecycle—from origination to repayment—enhancing efficiency and decision-making. Designed for both commercial and consumer lending, it supports personal loans, SME financing, BNPL, and more. Neobanks can leverage HES FinTech’s platform to launch and scale their credit services efficiently, optimizing loan origination, risk assessment, and compliance. With a 3-month TTM, lenders can introduce new credit products quickly while maintaining full customization control. Its cloud-based infrastructure ensures scalability, while seamless integrations with KYC providers, credit bureaus, and payment gateways enhance operations.

Offerings:

- Loan Origination and Management Software

- AI-Powered Credit Scoring

6. ProcessMIX

Here’s one more way to get a Neobank app – ProcessMIX low-code platform. ProcessMIX allows banks to build secure and high-performance applications quickly and within a moderate budget. The low-code platform facilitates banking app creation with an intuitive visual development interface, pre-made features (e.g., for calculations, rules, functions, etc.), easy integrations, and instant deployment on the AWS cloud. Using the platform, you can build a custom, full-functioning Neobank app in just a few weeks.

ProcessMIX utilizes AI/ML-powered automation for loan origination, risk management, complex calculations, security, and transaction processing. You can leverage the platform to modernize your existing applications with automation and security measures.

Multiple international banks have already benefited from using the ProcessMIX low-code platform.

7. Solaris

Solaris is a German SaaS provider of embedded financial services. As of 2025, Solaris powers over 50 FinTechs and Neobanks with modular solutions for lending businesses, payment processing, and account setup. The Solaris platform is fully compliant and has a robust KYC integration, making it the top choice among many European and international financial service providers. Besides, the company has a full banking license, which makes working with it a legally safe and predictable decision.

The features of Solaris software include:

- Cutting-edge Banking-as-a-service technology.

- Powerful APIs for smooth and frictionless connectivity and ecosystem growth.

- Cloud-based banking infrastructure.

- A data mesh architecture that supplies powerful data insights.

This way, working with Solaris gives FinTechs the combination of speed and flexibility of digital banking software with the benefits of a fully licensed bank.

8. Limepay

This Australian FinTech mainly focuses on merchants and making the merchant-customer financial relationship easier and more affordable. The company started as a standalone offer but today is requalified as a white-label solution. Today complete rebranding, incorporation of their solution is possible with the company’s vision of the future. While neobanking is not their main target, LimePay can become a part of a neobanking solution that allows for easy payments from within the app for a wide range of services.

9. Mbanq

This service is similar to RadarPayments since this is a platform that has all the features, tools, and possible solutions to launch an online cloud-based bank. Besides the fully customizable platform, a partner also gets a web banking app as a bonus. A testing environment is available for free on their website; it offers a sneak peek into the possible solutions one may get and a chance to test the compatibility of your technology with Mbanq. The features of this service range from loan configuration and accounts management to secure client management and advanced reporting. This is also a one-stop solution for a bank of any size.

10. Meniga

Being over 15 years in the market, Meniga has already won the hearts of many worldwide banks, such as ING Direct, mBank, or Santander, but it continues providing its white-label solutions to neobanks and customers directly. The company has a strong stand toward green initiatives; so for a customer, it offers cashback or help-the-planet solutions, while businesses can easily inform their clients about their carbon footprint and promote repayment. Meniga has a wide range of products to choose from: financial self-help for businesses and individuals (financial management assistance), aggregation of data, engagement strategies for driving customers and building loyalty, data analytics, personalized engagement strategies, and many more. The Meniga team knows its craft and has been winning FinTech awards almost every year since 2011.

11. Findity

Findity is a SaaS expense management platform for financial organizations and neobanks. One of the greatest benefits of this company is its care for the ‘paperwork’ related to local regulations. Whenever a team adopts Findity as their white-label solution and builds their own offer with it, all the legal matters get covered by the provider, regardless of the client’s country of operation. While working with every type of customer, including small neobanks and startup teams, Findity’s main focus is in the corporate world, where employers need a robust solution for accounting and payroll services. This means that this software can easily be incorporated into the day-to-day operations of any team, from a small niche challenger bank to a huge corporation with thousands of employees, and in both cases, it would benefit the client and its end-customers. If you are interested in a demo, Findity offers a tour around its solution here.

12. Penni.io

Online customer journeys for insurance products are the main service of Penni.io. The company has focused on providing a superb experience for the customers and an introduction to the world of online sales for neobanks. The team is constantly enlarging and improving to guarantee a smooth transition for end-customers and an intuitive way to sell insurance online. The main offer is a service that can be branded and incorporated into any existing platform or app to drive online sales of insurance packages. There is also a perfect front-end for customers to check out directly from the service.

The Bottom Line

Approximately 18% of American adults, as of 2025, have debt that they keep rolling over from one month to the next without significant reduction, based on the latest financial data. The number of loans made across the world has continued to increase, and so have outstanding loans. This has resulted in a 10% increase in world debt in 2024, and unpaid loans went up by 15% (IMF data). This is a trend demonstrating a continued and growing consumer need for innovative financial assistance and guidance to cost-effectively address their financial problems.

Neobanks definitely set future trends in the financial world. By making financial information, advice, and overall statistics available to every consumer with a tap on their mobile devices, these new financial institutions get closer to their end customers and provide a greater level of service than any traditional bank could ever imagine.

White-label solutions for neobanks help them reach their goal much faster. The existing software owners guarantee perfect customer service, fresh service, and convenience for the end-customer while also allowing to rebrand the software to be rebranded to match the bank’s marketing strategy. The market of software today is full of innovative ideas that can boost a neobank’s ROI or simply offer a platform for the development of a new financial solution. If you don’t know where to start, need help with implementing a solution into your daily operations, or have a 4IRE case that can benefit your team, contact us to discuss the details and begin transforming your offer today!

FAQ on white label solutions for neobanks in 2026

White-label software solutions represent ready-made, customizable software products meant for specialized goals (e.g., a digital wallet, a crypto bank, etc.). By buying a white-label neobank or renting it using a SaaS model, businesses can customize the platform’s design and offer banking services under their own brand without investing in expensive and lengthy custom software development.

Since the majority of core modules and elements are already built into a white-label software product, it usually requires limited customization work. Therefore, Neobank’s time to market may be effectively reduced to 2-3 months, compared to 6-12 months of full-scale Neobank creation from scratch.

White-label Neobanks usually come with the same set of services and features that Neobanks built from scratch, and support. Your product should provide core banking services, such as account setup and management, payment processing, card issuance, lending, and KYC/AML compliance. Some platforms are crypto-friendly and also provide an opportunity to buy, sell, and trade crypto assets.

Yes, reliable white-label products built by experienced software development companies are created with cybersecurity in mind. Thus, they are equipped with robust security protection, encryption, and advanced user access protocols that minimize the risk of hacker attacks and theft.

Yes, many white-label digital wallets and Neobanks come with the feature of cryptocurrency support. This feature may be introduced at the initial stage of Neobank development and launch or during later system upgrades.

-

Verified Expert in Blockchain

Verified Expert in Blockchain

-

16 Years of Experience

Similar articles

More articles