How to Start a Neobank in 2026: A Complete Guide

From what I have been observing in the FinTech market recently, I can surely say that the global banking sector has changed once and for all. The pace of progress is unstoppable, with all domains of human life transformed by technological innovation like blockchain and defi development services. Global finance is changing, and I see the following causes of this large-scale transformation:

- Public distrust in the global financial system’s integrity after the 2008 crisis.

- Quick introduction of digital, mobile, and other remote financial services during COVID-19.

- Growing financial inclusion of underbanked and unbanked populations with the help of digital banking and FinTech solutions.

As a result of these massive trends, new digital-only banks, referred to as Neobanks, digital banks, or challenger banks, have taken a fair share of the global market and continue to expand.

The service range of Neobanks is similar to that of usual banks, covering digital accounts, credit and debit cards, low-commission or fee-free transactions, loans, mobile payments, and currency exchanges. However, as they function beyond the traditional financial structures, their use is more accessible for unbanked populations.

New digital-only banks emerged recently based on such transformation of the financial landscape and broader adoption of technology. They are referred to as Neobanks, digital banks, or challenger banks, sharing a single common feature of digital-only service provision.

Here, I would like to share in-depth analysis of the neobank market and express my expert opinion based on many years of hands-on experience consulting clients and launching new neobank projects to uncover the ins and outs of Neobanking. Stay tuned to find out what it takes to launch your personal Neobank startup.

What is a Neobank? Famous Examples

So, what is a Neobank? In simple words, it is a financial institution that performs the functions and renders services typical for the usual brick-and-mortar banks, but in the digital-only format. Neobanks run without any offline branches and leverage technologies that are more advanced than in most banks. A standard range of Neobanks’ services includes accounts for individual and corporate clients, credit and debit cards, mortgages, loans, deposits, and individual payments.

The present-day differentiation of bank types has led to significant confusion about their differences and similarities. Here is a brief recap:

Traditional Banks are the physical banking establishments, government- or private-owned, serving the population with a range of conventional banking services, such as account opening, deposits and loans, credit and debit cards, and financial transactions.

Digital Banks are backed by large financial institutions but rarely have offline offices and rely on online banking mostly. Most services are rendered via mobile or desktop apps.

Neobanks fulfill the same functions as digital banks, but they are not backed by any large financial organizations like conventional and digital banking. Most of them are launched by private organizations and pursue the online-only model of service.

Crypto Banks are blockchain-based institutions functioning beyond the regular scope of banking. Such banks are not necessarily tied to any fiat currency. Often Crypto Banks function on the edge between fiat banking and crypto world.

The spread of Neobanks is large-scale, with such institutions emerging all over the world and currently serving over 500 million users. The highest percentage of financial services’ adoption is observed in Asia and developing countries, with large numbers of unbanked or underbanked people. Here are a couple of famous Neobank examples.

- Revolut – a UK-based Neobank launched in 2013 and currently serving 15+ million users. At present, the bank handles 100+ million transactions every month and provides services to individuals and businesses.

- WeBank, Inc. – China’s first digital-only bank created in 2014. The bank is backed by Tencent and offers a wide variety of financial services to unbanked populations.

- Alipay – China’s Neobank focused on making digital payments accessible for everyone and. It covers a broad range of payments and digital services in China and allows frictionless mobile payment solutions for individuals and businesses.

- Nubank – a Brazilian Neobank that occupies a leading place among Latin American neobanks. It has over 80 million users in Brazil and over 1,5 million users in Mexico and Colombia. The company’s market cap by the moment of its IPO in 2021 was $45 billion, and in 2023, it was ranked as the #1 Brazilian bank.

- Chime – a FinTech service provider with an easy online banking experience and the absence of monthly service fees. Users can open checking and savings accounts, receive secured credit cards and enjoy convenient digital banking services via the broad network of this San Francisco-based neobank’s partnerships.

- Wirex – an example of crypto/fiat crossover, an all-in-one app for crypto transactions and a digital payment platform. It’s a new form of Web3 money app, which shares the features of usual digital banks and new, blockchain-powered functionality

Overview of Neobank Market Size

The Neobank sector has grown significantly since 2015, mainly due to the rise of demand for flexible and more accessible financial services among masses of the unbanked population. To date, there are over 400 Neobanks registered across the globe, serving over one billion users in both developed and developing countries. Though such non-conventional banking services are popular in all parts of the world, the highest adoption levels for Neobank technology are observed in China (93%), India (50%), and Brazil (32%). So, businesses considering a Neobank launch have good chances to get a fair share of the rapidly developing market with accelerating growth and multiplying revenue streams.

I’ve been witnessing rapid alternative banking development over the past decade, with the trend accelerating during COVID-19. In part, such trends are explained by the growing disappointment of users with conventional banking complexities, resulting in a search for simpler, less expensive solutions. Besides, massive numbers of the unbanked population get access to finance via Neobanks, thus further fostering this DeFi niche.

Just look at these stats:

- Transaction value in the neobanking market exceed $6.3 trillion in 2024.

- The 2023 market cap of Neobanks is $98.4 billion.

- The CAGR of this market is over 48%, which is likely to let the market exceed $3.4 billion by 2032.

There will be over 386 million active users of Neobank services by 2028, according to Statista.

Features of Neobanks

An essential feature of Neobanks one should consider first is the absence of physical offices and branches. Such banks function in the digital-only or app-only format, making such financial institutions more cost-efficient and optimally structured. As a result of spending less money on office rent and salaries of numerous office staff, Neobanks can deliver financial services at a lower cost, with their clients incurring lower fees and commissions.

Second, all Neobanks utilize innovative financial technology, such as innovative payments processing, convenient mobile apps, flexible back office solutions (including KYC, AML and transaction monitoring), real-time balance and transaction status updates that power their apps and platforms. As a result, the financial services become faster, securer, and more accessible to populations on the go. Everything can be done in a couple of clicks, with users undergoing simplified verification procedures and enjoying intuitive, easily navigable interfaces of their Neobanks.

Third, you need to keep in mind that though there is a word “bank” in the term “Neobank,” technically, many of them are not banks per se. Many Neobanks don’t even hold banking licenses required for such type of activity. It doesn’t mean that non-licensed Neobanks are scams or frauds; the only concern you might have about this is that central national authorities do not regulate such institutions. Thus, your affairs with that institution are more of a private contract nature.

Overall, Neobanks are currently not meant to substitute the banking system altogether. Instead, they are an alternative for people seeking quick, affordable, and flexible solutions for commission-free or cheap transactions and personal/business accounts with low maintenance fees. The standard set of services rendered by Neobanks includes:

- Cards issuance (plastic, virtual)

- Savings features

- Credit

- Conversion fiat/ crypto

- Cross-border payments including in crypto

- Budgeting assistance

- Push notifications.

- Contactless and QR code payments.

- Personalized and user-friendly banking services.

- Advanced cybersecurity measures.

Because Neobanks are not licensed in most cases, they cannot provide insurance for the clients’ deposits and can’t give credits and loans to the population. However, some Neobanks have closed this gap by partnering with traditional banks for insurance and credit guarantee provision. Thus, clients of such financial establishments should first check all the available documentation to see their protection and guarantees.

As a result of added flexibility and lower commissions, Neobanks are known to achieve some unique benefits currently unattainable for traditional banks:

- 24/7 access to the entire service range

- Ability to create a multi-currency account in no time

- Ability to conduct operations at any time, from any place, on the go

- Open technical infrastructure enabling hassle-free, plug-and-play user experiences

- Customer-oriented services and UI/UX

- Full financial visibility (all your credit cards and accounts all in one place)

- No fees for spending or transferring money abroad

- High-level protection from card fraud and identity theft and more.

Unlock Financial Freedom with DeFi Innovators

Ready to redefine finance? Empower your business with decentralized finance solutions crafted by our seasoned team. Schedule a free consultation with our seasoned expert today!

Strategy for Neobank Development

Once you’ve decided to launch a Neobank, you need to develop a detailed plan and strategy first. A recommended path for strategizing for a new financial product is determining a problem and working out a value proposition to address that problem. For instance, you notice high transborder transaction fees in your region and come up with an optimal solution that reduces fees and creates optimal, safe transaction services for clients. Describe in detail what value your company will bring to clients and approach the development of your Neobank’s technical specifications with these projected functions in mind.

Determination of the problem your Neobank will solve is impossible without understanding your clients’ needs and issues. To comprehend them well, you need to develop a customer profile, thus matching your unique USP with the clients’ pains and gains.

Next comes the development of a minimum viable product (MVP) and its field testing. Dedicate exceptional attention to testing your business model at this early stage of Neobank development. It will disclose the idea’s vulnerabilities and inconsistencies to address early in the development cycle. Test the idea against operational, financial, and commercial aspects of Neobank’s operation to see how well it matches the market demand and client requirements. Once these criteria are considered and field-tested, your business model transforms into a business plan that can go further through the software development pipeline.

What to Consider Before Developing a Neobank?

Don’t forget that your Neobank app is a digital banking service. Thus, it will deal with user money and private, sensitive information about account holders. These procedures should be organized in line with the relevant jurisdiction’s regulations and laws and with proper respect to cybersecurity. I recommend prioritizing these aspects:

- Compliance with the PCI DSS standard that guarantees the security of digital transactions during card payments.

- AML/KYC procedures for the absence of legal risks and allegations of money laundering or support for terrorism or criminal activities.

- Customer data protection (GDPR or other laws relevant to your bank’s jurisdiction).

- Licensing is optional for Neobanks, but having a license increases your project’s reputation and trust.

It’s also important to take proper care of the technological interoperability of your platform. It can be ensured by cross-platform tech stack – Android and iOS usage for mobile app creation – and the application of universal programming languages and frameworks like React Native. Finally, a robust cybersecurity shield from hackers and criminals will add technical superiority to your platform, giving you and your users peace of mind.

Monetization Strategies for Neobanks

Neobanks are different from traditional banks in terms of monetization, so you can explore a broader range of revenue streams for your new project:

- Lending services. Many Neobanks provide loans to clients based on smarter, AI-powered credit risk evaluation mechanisms. As a result, they derive revenue from interest rate from loans and credit card usage.

- Ecosystem fees. Neobanks can establish a broad variety of partnerships with other service providers and get revenue from users’ payments for subscriptions, streaming services, food, and other elements of a broader Superapp ecosystem.

- Asset management. This scheme is a golden standard in the banking industry; it lets Neobanks strike the right balance between deposits and loans on competitive terms and represents an ethical monetization model.

- Partner commissions. Many tech companies partner with Neobanks to take advantage of the product extension monetization model. You can also engage other services via APIs and negotiate commission fees from the products users pay from their accounts or cards.

Neobank Development Step by Step

The process of creating a Neobank may look complicated and confusing at first. However, based on my experience in this niche, I want to reassure you that a systematic approach makes a real difference. When you’re working with an expert team with advanced FinTech training, it all boils down to a clear algorithm of 7 steps.

Step 1. Market Research and Discovery

This initial phase involves an understanding of the market you plan to operate in. It refers both to the competitor analysis to identify your unique USP and business value and the market research for grasping compliance and jurisdictional nuances.

By the end of this stage, you should already have:

- A target operating model.

- A plan of compliance with the national financial regulations (a full banking license, a FinTech-only license, or the partnership model).

- A clear vision of your Neobank’s processes and activities.

Step 2. Assembling a Skilled Team

Next comes the partnership with a skilled development team that will perform all technical tasks, starting from project specifications, UI/UX, and the bank’s actual development. I recommend thinking about this stage early on, as the skill and tech expertise of your developers can make or break your Neobank. Thus, you should find a development agency with a relevant tech stack, a sufficient number of available employees, and an in-depth understanding of your FinTech niche.

Step 3. Design

The following stage is UX/UI design, which is a vital part of the project. You need to have a finalized version of the design before proceeding to development, as it will become your programmers’ roadmap. The design and development phases are tightly linked with each other, affecting the functionality and effectiveness of the final software product.

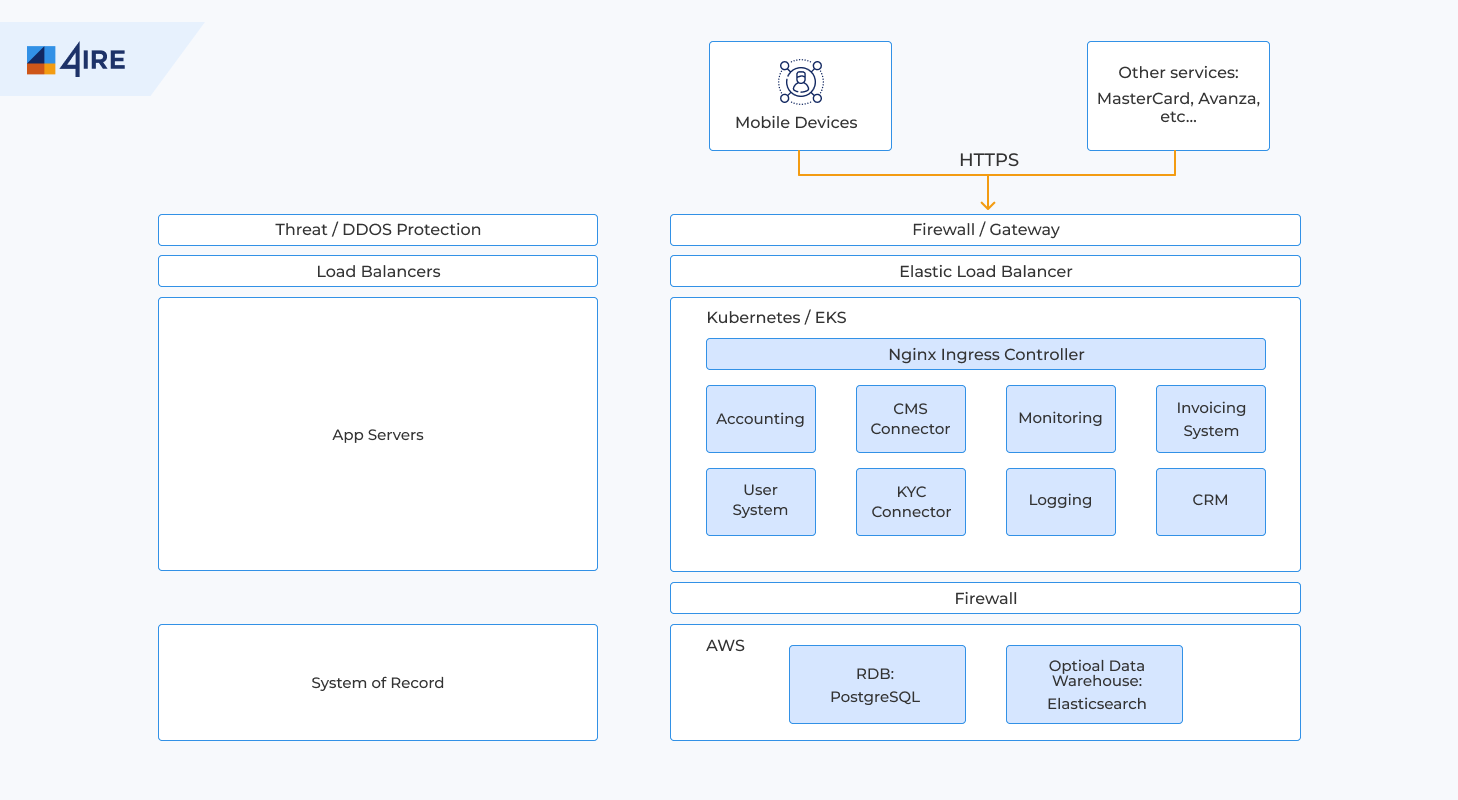

Step 4. Development

Once the design and UI/UX aspects are clear, it’s time to proceed to software development. Creating a well-functioning back-end is the most critical task in this process. It comprises the core of your banking app and regulates all processes conducted by clients and administrators within the system. Existing core banking solutions for banks, such as Mambu, Temenos, or IBM, are pretty popular among traditional banking institutions, but they are often too costly for startups on a budget. Thus, it’s preferable to stick to custom development solutions fitting your startup scale but allowing further scaling as your business grows.

Front-end is also a critical element of Neobank development as it contributes to user satisfaction and shapes positive customer experiences. Handy payment gateways, intuitive interfaces with minimal input from the user, mobile and online banking channels all shape positive user acceptance and heighten customer loyalty to your product.

Step 5. API Integrations

The development of the API layer is vital for any Neobank’s functioning as APIs unite your platform’s internal processes and services with external applications. Neobanks don’t function as separate, isolated systems; most of them thrive due to effective cooperation with other financial actors and the provision of multi-agency services. Thus, having a third-party API layer allows a Neobank to set up partnerships with other market participants, such as allowing transactions of funds to other providers, collaborating with external card issuers, partnering with physical banks for credit loans and insurance coverage, and the like.

Step 6. App Testing

Once the neobank’s software is ready, you need to complete a thorough audit of the code logic, bugs, and vulnerabilities. I advise doing both manual and automated QA tests for the created platform, as they can give different perspectives on its weaknesses and strengths.

Step 7. App Deployment and Updates

Once all the bugs are corrected upon the QA testing results, your neobank will be ready for deployment. However, it’s not the end of the project; instead, it’s the beginning of a long-term partnership with your development team that will conduct maintenance and introduce vital system upgrades.

Reasons for Neobank failure

Once the strategy is ready, and a team is set up, you might think that your Neobank project is doomed to success. However, it’s frequently not the case as your Neobank can face several challenges, which sometimes even lead to the project’s failure. The reasons why your project may fail or under-deliver include:

- Financial issues

The primary purpose of a Neobank is to generate revenue for its creator, so many clients expect incredible returns in the first years, if not months, of their project’s operation. In fact, a financial project like Neobank needs time for maturing and winning its loyal customer base to generate stable revenue streams. Even digital banks with a name in the industry have experienced financial problems, such as a lack of investment or insufficient investor funds at critical project stages. So, it’s better to have a detailed financial plan to avoid such emergencies.

- Regulatory problems

Though representing an alternative to conventional finance, Neobanks should still comply with regulations of their relevant jurisdiction. Neobanks should implement rigorous security measures, conduct user authentication, and hold continuous financial monitoring, which requires extra resources and technical features.

- Stringent competition

The Neobank industry is still in the germinal stage of development, with the 2020s being a momentum for its acceleration. However, Neobanks started emerging over two decades ago, and there are a handful of strong national and international market players in most regions today. New Neobanks may find it challenging to differentiate their business USP and win a share of the existing customer base.

- Vague expectations

A lot of problems with Neobank project implementation comes from the vagueness of requirements or confusion regarding the project’s strategy, values, and goals. If there is disagreement in the client’s board of directors or team responsible for Neobank development, the project may stagnate until a consensus is achieved.

- Expensive software development

Software costs are mounting year by year, especially in the trending blockchain and DeFi industry. Thus, clients wishing to join this niche and reap the benefits of the emerging DeFi market need to spend substantial money on software development. At times, the development process gets interrupted if the development budget exceeds the initially agreed one and the client lacks funds for its completion. To avoid such a situation, you need to stipulate all costs and expenditures in a contract with your software development provider, preventing hidden costs and budgetary vagueness.

How We Can Help

Once you’ve made up your mind to set up a Neobank, it’s time to find a reliable, experienced software developer for the task. The 4IRE team of fintech developers and software engineers is at your service, offering 10+ years of DeFi expertise and an extensive tech stack for smooth and cost-effective Neobank development.

Our company partners with many large banks to guarantee a smooth head start for your Neobank project in the market. I have personally launched such projects from scratch and led them to the first 100,000 users, so 4IRE is really a place to get a turnkey Neobank service. We can also speed up the entire development and launch process with the help of the proprietary ProcessMIX platform for low-code back-end creation.

Our experts have dozens of successfully finalized DeFi and FinTech projects, able to design custom solutions in line with your individual business needs. Talk to 4IRE managers today to discuss the project and get a quote; you may be just a footstep away from an innovative, user-friendly, and lucrative Neobank.

FAQ on starting Neobank in 2026

The modern global finance industry is getting increasingly digitalized. That’s why you can benefit from a neobank as an innovative, digital-only banking product. Users are adopting digital banking solutions at a faster pace today, which creates an optimal moment for digital bank development and launch today.

There are many strategies for turning your neobank into an additional revenue stream. You may provide deposit and credit services to clients, integrate your banking solution into a larger financial ecosystem for a lucrative commission, derive revenue from advertising and promos, and engage in profitable partnerships with other businesses.

The main determinant of your neobank’s cost is the project’s complexity and number of features. A simple app may cost from $40,000 to $60,000, while a highly complex neobank will already exceed the $100,00 mark. Depending on the location of your team, you should expect to pay anywhere from $40,000 to $250,000+ for this software product.

The timing, as well as the cost, of your neobank depends on the project’s scope and complexity. Besides, it differs depending on the team’s composition. As a rule, software development projects are calculated in hours, and the size of the team will determine how quickly it will cope with all tasks. On average, you may need from 3 to 8+ months for building a neobank from scratch and launching it.

4IRE is one of the indisputable leaders in the mobile and digital banking development niche today. We have an extensive developer team, many years of experience in the banking niche, and a proprietary low-code platform, ProcessMIX, that accelerates the neobank’s development and launch processes.

Similar articles

More articles