Make Better Decisions with a Reliable Credit Scoring System

Table of content

To get a loan, borrowers have to prove that they are reliable, trustworthy, and able to repay the debt in due time – in short, that they are creditworthy. Thus, the lenders issuing loans need to double-check the borrowers’ characteristics carefully. Every wrong decision can cost them money if the borrower fails to repay the debt and goes bankrupt.

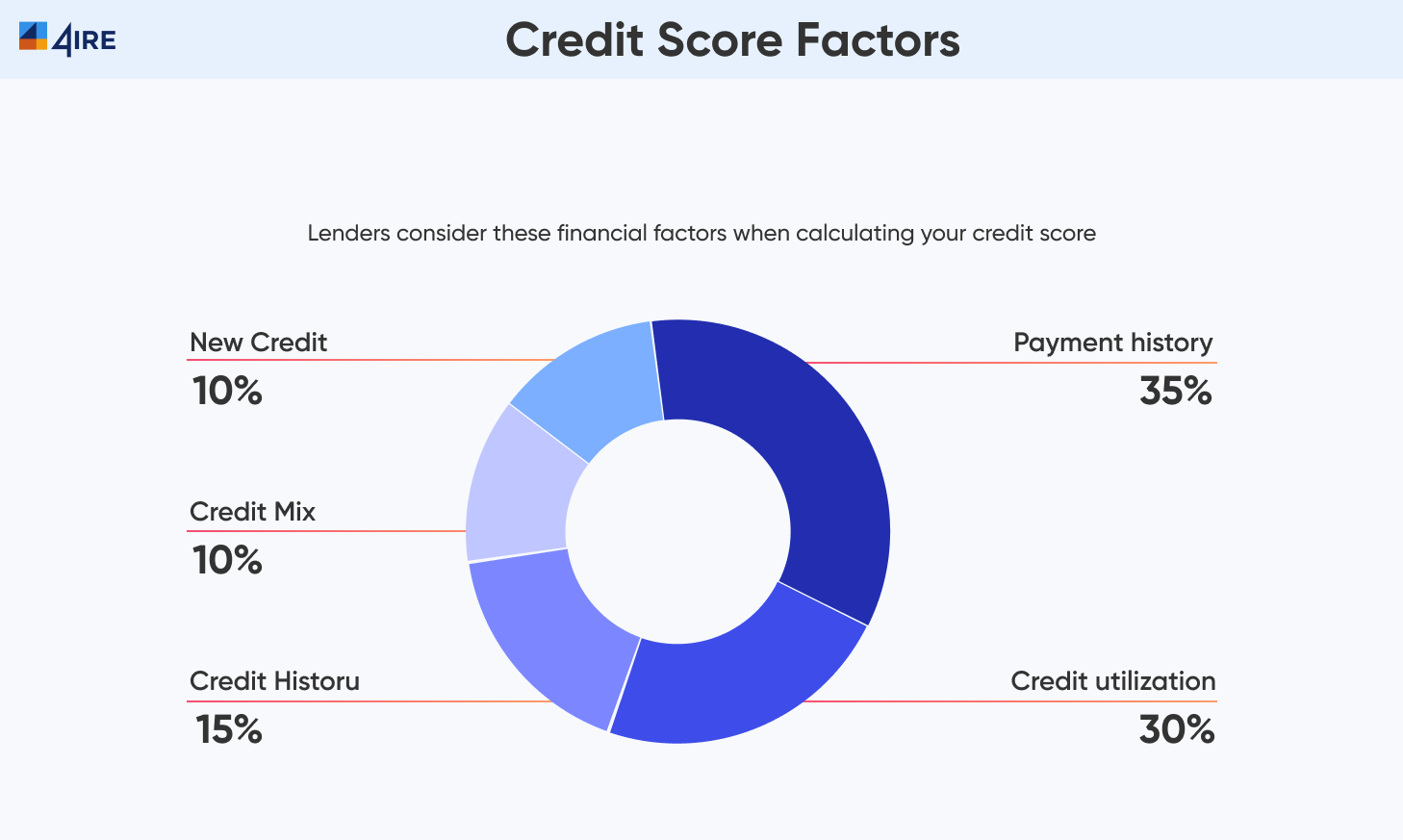

The best instrument for assessing the borrower’s trustworthiness is a credit score. This compound score is calculated based on a complex set of borrower characteristics. These characteristics include their past loan performance, income, employment, socio-demographics, and many others.

Yet, the traditional credit scoring approach is gradually losing its relevance. It relies only on the past and current data about borrowers, failing to consider their potential revenue and business success in case of a positive loan decision. Reliance on historical data has left over 1.2 billion people worldwide without access to financial services, and new credit-scoring approaches have emerged to solve this problem.

Here I examine the modern credit scoring approaches and consider the opportunities for forward-looking businesses, from digital banking to Neobanks and crypto banks, to expand their customer base without incurring high credit risks. With this information at hand, you can set up a smart credit scoring system deriving data about borrowers from multiple channels and making more informed loan decisions to balance business revenue and finance access democratization.

Credit Scoring Trends in 2022

It’s not enough to know the credit scoring system definition to set up a workable algorithm for credit risk assessment. The financial services landscape evolves very fast, and you need to keep pace with the latest trends to offer your customers the best service, reduce credit-related risks, and generate greater profits for your bank.

Expanding AI Use for Better Credit Scoring Decisions

The pace of AI and ML adoption in financial services is accelerating, as these technologies can automate credit risk assessment and simplify decision-making. With innovative AI-based systems, companies can expand the scope of potential borrowers, including even those who lack traditional credit scores, which increases user trust and satisfaction. Besides, AI algorithms add flexibility to the credit terms and decisions, allowing borrowers to understand what parameters affect their applications’ outcomes.

Considering Data from Multiple Sources

The recent lending crisis resulting from the COVID-19 pandemic and related business downtime showed how dangerous it is to rely on a single data source and historical credit records of borrowers. The modern FinTech product use trends suggest the need for new credit scoring approaches. This also allows for incorporating a broader range of user data from multiple channels, giving more precise insights into the customer’s ability to repay debt.

Broadening Access to User Data for Financial Institutions

The major bottleneck for receiving a loan has always been a lack of past credit history. With the advent of PSD2 in the EU and the proliferation of Plaid in the USA, individuals have received additional opportunities for lending by giving banks access to their consumer-level data. These regulatory arrangements enable people to grant access to their spending data to financial organizations, thus allowing the lenders to assess their reliability and evaluate the credit risk more precisely.

The Rising Role of Data Analytics in Credit Scoring

Big data about everyday consumer behavior and spending habits is an invaluable source of information for credit scoring decisions. Therefore, financial organizations employing AI and ML algorithms for big data analytics are better positioned in credit risk evaluation and comprehensive borrower profiling.

Ready-Made Credit Scoring Solution vs. Custom Credit Scoring Solution

There are many possibilities for setting up a credit scoring system for your financial solution. You can choose between plug-and-play products available on the market or opt for the development of a customized solution from scratch. Here are the pros and cons of each option.

| Ready-made credit scoring solution | Custom credit scoring solution |

|---|---|

| Low cost | The price of custom solution development is high |

| Quick time to market and speedy integration | Custom credit scoring system's development is lengthy |

| No specialized qualification is needed for the solution's setup | You need to hire a professional team to create a cutting-edge credit scoring system |

| Additional features come at an extra cost or even impossible to implement | Custom solutions are scalable and flexible |

| The solution is not unique, which minimizes your competitive advantage in the financial services market | A unique mix of credit scoring parameters allows you to outperform the competition |

Credit Scoring Software Solution: How to Build One?

Creating an innovative credit scoring system is a lengthy and complicated task. So, it would be best to do some preparatory work on strategy development to ensure that the new element of your IT infrastructure is consistent with the rest of tools and procedures.

What should you consider when building a credit score solution?

Before embarking on the software development project, you need to:

- Determine the goals you wish to attain with this system’s implementation (e.g., rising revenue, expanding the customer base, reducing the number of bad loans)

- Indicate the data sources from which you will compile the customer’s risk profile

- Select AI and ML tools you want to integrate into the system

- Define ways to align the new system with your existing risk management infrastructure

Include these specifications in the technical task for your financial software developer. This way, you will avoid confusion and guarantee that you receive the software meeting your business needs and expectations.

Unlock Financial Freedom with DeFi Innovators

Ready to redefine finance? Empower your business with decentralized finance solutions crafted by our seasoned team. Schedule a free consultation with our seasoned expert today!

Credit Scoring Software Benefits

Automated credit scoring solutions are a significant step forward in improving your financial organization’s performance and speeding up loan-related decisions. First, it eliminates the need for, time, and cost of manual credit scoring and processing. Second, automated software can help you perform a more comprehensive assessment of your borrowers’ creditworthiness. Third, it will optimize the processes involved in risk assessment and credit terms’ formulation, thus increasing your customers’ satisfaction with the speed and quality of service. Other benefits of automated solutions are:

- Higher quality and precision of lending decisions

- Higher transparency of the credit scoring process

- Customer satisfaction with the speed and clarity of the decision-making approach

- Greater customer outreach with lending services

- Customer base expansion for higher organizational revenue

- Optimization of the loan disbursement pipeline

These improvements come with advantages on the organizational and client side, with better control of data and more comprehensive data management coupled with higher customer satisfaction. Therefore, using automated credit scoring solutions is a wise decision today, amid the rising demand for lending services, diversifying credit risks, and the need to implement big data analytics.

Credit Scoring Software Implementation

Once you have chosen the credit scoring software for your financial institution, it needs to pass through vital implementation stages, becoming a part of your IT infrastructure.

#1 Population Segmentation

The first stage of the credit scoring system’s use is the selection of specific population categories and assigning credit score calculation parameters to each of them. You will have different methodologies for credit risk calculation for the elderly versus students, employed versus unemployed, etc.

#2 Credit Score Calculation

This stage involves using numerous data sets for a comprehensive and precise credit score formation for every lending product and every borrower. One can set up an algorithm for deriving data from external sources (e.g., credit bureaus), digital channels (e.g., big data analytics with AI and ML algorithms), and any other data sources including Open Banking data.

#3 Scorecard Choice

Next, you should specify the type of scorecard you will apply in credit-related decision-making. At present, three options are available: statistical (past credit data-based), judgmental (expert judgment-based), and hybrid (a mix of both).

#4 Scorecard Design

At this stage, you need to determine the settings for every scorecard defining high and low risk, determining bad and good loan conditions. The decision for each borrower will be made based on the combination of these settings.

#5 QA Testing and Implementation

It’s wise to back-test your scorecard design and check the system’s safety and reliability before launching it. The QA results will give you workable data for final revisions, allowing you to avoid risks and set up a well-functioning credit scoring system without friction. Moreover, one can also use back-testing based off existing data on both borrowers and loan outcomes.

#6 Regular Updates

You will achieve much better outcomes if you update the credit scoring system based on historical data and statistics. You can schedule updates once a month or a quarter, analyzing its output in both positive and negative loan decisions’ correctness.

How Does Credit Scoring Affect Bank Profits?

Implementing a new credit scoring system can boost the bank’s profits in many ways. First, it introduces automated solutions and increases the speed of credit scoring, thus saving human resources and improving customer satisfaction. Second, such a system can deliver consistent data for more precise decision-making, thus minimizing the number of bad loans. This change increases the operational efficiency of financial institutions and reduces the cost of vital services (mortgage, car loan, or business loan). Third, the cost income ratio (CIR) rises with better risk management and bad loan ratio reduction. CIR increases are always good as they make banks more attractive for investment. In the end, banks have better control over risk and cost allocation, reducing the number of client bankruptcies and maximizing business revenue.

How Credit Scores Can Improve Risk Assessment

In a nutshell, credit scores help a financial institution calculate the probability that their borrower will repay the loan on time and without trouble. Therefore, a precise and well-customized credit scoring system can help you:

- minimize the number of risky loan disbursement

- automate the credit assessment procedures

- reduce the number of wrong decisions

- decrease business losses due to wrong credit decisions

- expand the customer base without elevated risks

- shorten the risk assessment process, adding to client satisfaction

- optimize the credit risk assessment algorithm without additional human resources involvement

You gain a sustainable competitive advantage in the financial services market by achieving all these outcomes. On the one hand, better risk assessment methodologies allow you to reduce the number of bad loans and increase business profitability. On the other hand, you can attract more clients by giving more flexible loan terms and ensuring broader population coverage with lending services.

Conclusion

The financial services market is evolving quickly, and the competition gets fiercer day by day. Only those who deliver cutting-edge solutions to clients and calculate risk precisely can stay afloat and survive. Therefore, by implementing an innovative and smart credit risk scoring system, you can minimize the losses and increase the performance of your credits. You can win a fair share of the booming FinTech market by applying blockchain, AI, and ML technologies. So, use the tips and implementation steps discussed above to advance your financial business’s performance and serve your clients better.

FAQ

As a rule, mortgage lenders utilize the FICO score for calculating the mortgage terms for individuals. FICO is an acronym for a data analytics company Fair Isaac Corporation, which covers over 90% of lending decisions in the USA. Another option is the Vantage Score – a leveraged data analytics provider making credit more accessible to people invisible to the traditional lending market. FICO scores 2, 4, and 5 are used in mortgage loan decision-making.

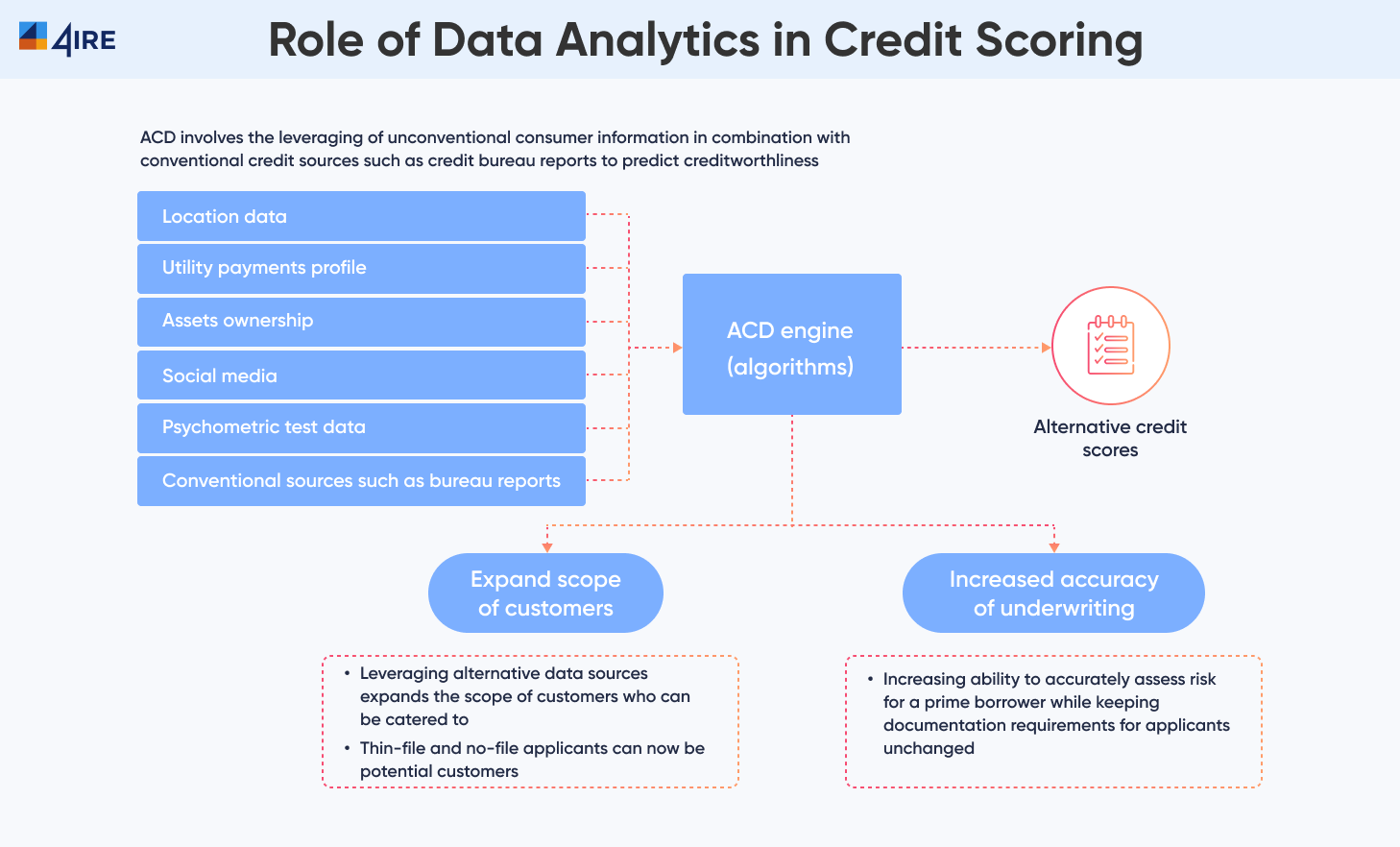

Alternative credit scoring is a new approach to the calculation of credit risk. It addresses the lack of reliable data about borrowers in the public credit registries, which is common in emerging markets, and issues credit risk profiles based on big data about users. This way, lenders can decide on loan disbursement based on the data from users’ rental payments, utility bills, consumer behavior, and other non-banking sources of data about their financial behavior.

The recent technological advancements have brought much innovation in calculating lending risks. Previously, lenders could derive the information about their potential clients only from the official banking data and credit history. Now, they can utilize multiple user data channels, ranging from digital profile (browser used, type of device, geolocation, VPN use, etc.) to ML scoring. These data sources help create a more detailed borrower profile and calculate risks more precisely, thus giving more people access to the lending market.

The traditional credit scoring approach is based on the borrower’s credit scorecard, that is, their past credit history. It also considers the client’s socio-demographics, including their age, gender, occupation, marital status, and the number of family members. However, this method has limitations as it prevents access to the lending market for new clients without a credit history. Second, it doesn’t take into account the revenue prospects of young borrowers based on their education, investment activity, etc. These characteristics are included only in more innovative, ML-based credit scoring algorithms.